It's a fix - part 1

Local electricity pricing isn't all it's cracked up to be

“Market failure” often means “market outcomes I don’t like”, and “market improvement” often means “skewing markets to try to make them produce outcomes that I approve of [/in my interest]”. Unless the market improvement is removing obstacles to voluntary exchange, it reduces efficiency by definition, because no institutional change would have been required to make markets gravitate towards outcomes that are more cost-effective and not institutionally-inhibited.

The justice of the improvement lies in something other than an increase in utility. Typically, it consists of the circular logic of (a) calculating the “efficient” solution, (b) finding that the market doesn’t agree, so (c) trying to make the market deliver it in order to promote efficiency, which is morally-desirable. Costs to customers and taxpayers (including the costs to encourage these “efficient” outcomes) often rise, but that is no discouragement to people who know that their calculations must be more accurate than market discovery.

Policy Exchange (PX) have a number of ways they think we should improve the electricity market:

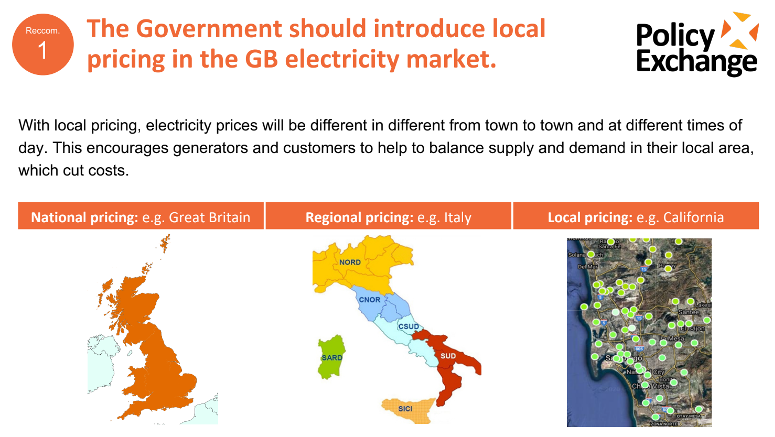

“Local pricing”

“Floor-price Contracts for Differences”

A “low-carbon quota” for the Capacity Market

This is the first of three posts looking at each of these claims in detail.

Local pricing

In quantifying that cost, PX (not Aurora) resort to the classic device to make small numbers look bigger. It will save £50bn, they say, so long as you add up all the prospective savings between 2026 and 2050. Yes, and I earn over £1,000,000, so long as you add up my earnings over the course of my working life. It’s an annoying little propaganda technique that is a reliable pointer to people trying to spin a narrative.

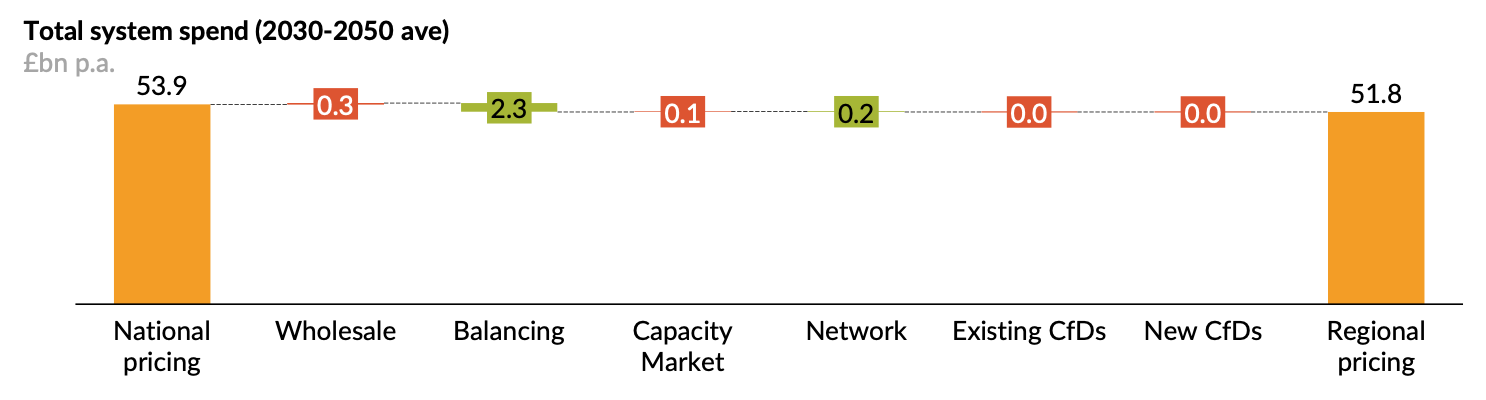

£50bn isn’t even justified by the Aurora report. They estimate an average of £2.1bn/year between 2030 and 2050, i.e. £42bn. PX have to move the boundary to that rather odd starting point of 2026 to get their nice, big, round number. But that assumes the costs can be backdated like that. Given the scenario modelled by Aurora, it’s a fair bet that the costs are back-end loaded, and the savings at the start of the period are lower.

Still, savings sound great; but relative to what? It’s a reduction in the projected average electricity system spend between 2030 and 2050, from £53.9bn to £51.8bn p.a. Aurora do not define electricity system spend. Does it include taxes, for example?

Like most British statistics that actually matter, it is surprisingly hard to find a figure for current electricity system spend. But if we apply average prices to the UK’s sectoral electricity-consumption figures, we get a rough figure of £45bn. Aurora’s figures appear to be in constant £2012 (though it is not clear). £45bn in £2019 would be more like £40bn in £2012. And we know the £45bn includes tax, margins, etc, which we don’t know for sure about Aurora’s figures.

In other words, this reduction of £2.1bn/year is probably an increase in real terms of at least £10bn/year. But at least it’s less than the increase of over £12bn that would otherwise occur. The report would have had a different tone if expressed that way.

How can local pricing save cost, you might well wonder? If all it did was substitute local prices for national prices, with no change to the underlying distribution of supply and demand, then all it could do would be to redistribute cost, not reduce it.

One effect of “local pricing” has nothing to do with its localism. They have wrapped a hotter political potato in a cosy communitarian blanket. They assume local pricing will include time-of-day pricing (“Half-hourly demand within each zone is flexible, as EVs, heat pumps and electrolysers respond to regional pricing”). In other words, electricity will be cheap when demand is low and there’s plenty of supply (e.g. summer nights) and expensive when demand is high and supply is tight (e.g. winter evenings, though that becomes much less predictable with a lot of intermittent generation on the system).

The expectation is that customers will reduce their demand when prices are high and try to concentrate their demand on cheap periods. Persuading people to cut their consumption when it’s cold, dark and still outside would undoubtedly save cost. There’s no reason this wouldn’t be equally true for time-of-day pricing under a national pricing model, but that does not seem to be one of their modelled scenarios.

Time-of-day pricing is the right approach. The current approach to pricing is inefficient. But people are generally not keen on being exposed to reality through the pricing mechanism. So it is politically unpopular. That is presumably why a change that depends on “demand-side management”, as it is known in the industry, is being dressed up as localism.

There is a problem with disguising the truth. It might help to sneak legislation through with less opposition, but it can’t disguise the effect when implemented. It treats the public as fools to be hoodwinked rather than intelligent people owed an honest explanation by their representatives. It diminishes trust, inhibits reasoned discussion, and reduces the chance that people will come to understand the uncomfortable truth rather than reaching for comfortable fallacies. It is classic British Establishment. It is the reason why our governance is so dysfunctional. It reveals the intellectual insecurity of the people who think themselves sufficiently superior to take this course – if they could justify their choices, why wouldn’t they declare them openly?

In Aurora’s explanation, almost all of the saving comes from “Balancing spending decreases”. Demand-side management driven by time-of-day pricing will have that effect. But they focus on “the reduction in constraint costs as regional pricing introduces a signal for RES, particularly in Scotland, to curtail.” There are reasons to be sceptical that this is as significant as demand responses.

Curtailment means reducing the output below the level that could be produced at that moment. The curtailment of wind and solar saves almost no cost. It moves it. Their marginal operating cost is close to zero, so curtailment has a minimal impact on their costs. It reduces the number of MWh over which their mostly-fixed costs can be spread, which means they would have to achieve higher prices at other times, or reduce their returns, neither of which is a real saving.

There is no particular reason why national pricing should not also send signals to RES to curtail. It already does. In fact, one of the drivers for PX’s report was the increase in system balancing costs under Covid, which highlighted (through a fall in demand) the challenges and costs of balancing demand with increasing levels of intermittent power. A key part of that cost is constraint payments, whose increasing cost has been highlighted by the GWPF.

In fact, curtailment incurs cost. Almost all the cost of wind and solar is incurred regardless of how much they are curtailed. But the more they are curtailed, the less they are contributing to total annual supply. Assuming total supply remains constant, that means that other sources must be contributing more in total than they would have been had intermittents not been curtailed. This is the inverse of the argument often made for intermittents: they may not reduce the capacity of fossil-fired generation that we need on the system, but they reduce their utilisation. If the intermittents are curtailed, we must be using the fossil-fired capacity more than would have been the case without curtailment.

It is not persuasive that the main cause of reduced balancing spending is increased curtailment in Scotland, especially when we have a credible explanation for it in the unheralded inclusion of time-of-day pricing. When we look at the modelled effect on the deployment of intermittents, it seems even less likely that the cost saving stems from their utilisation levels.

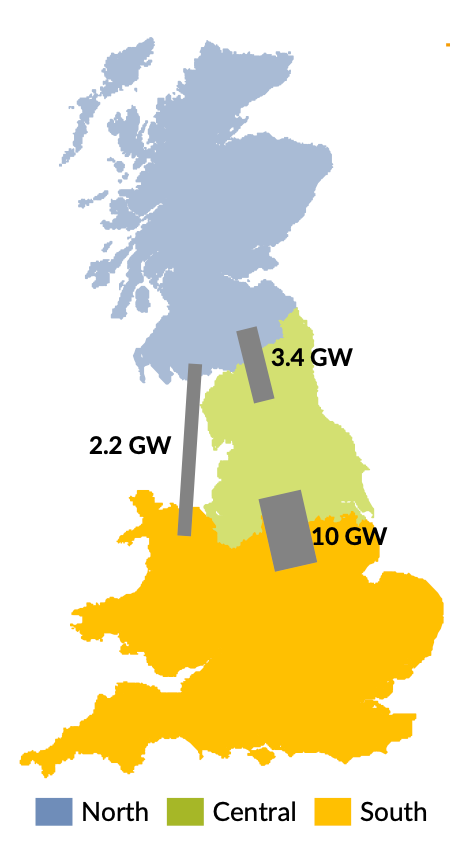

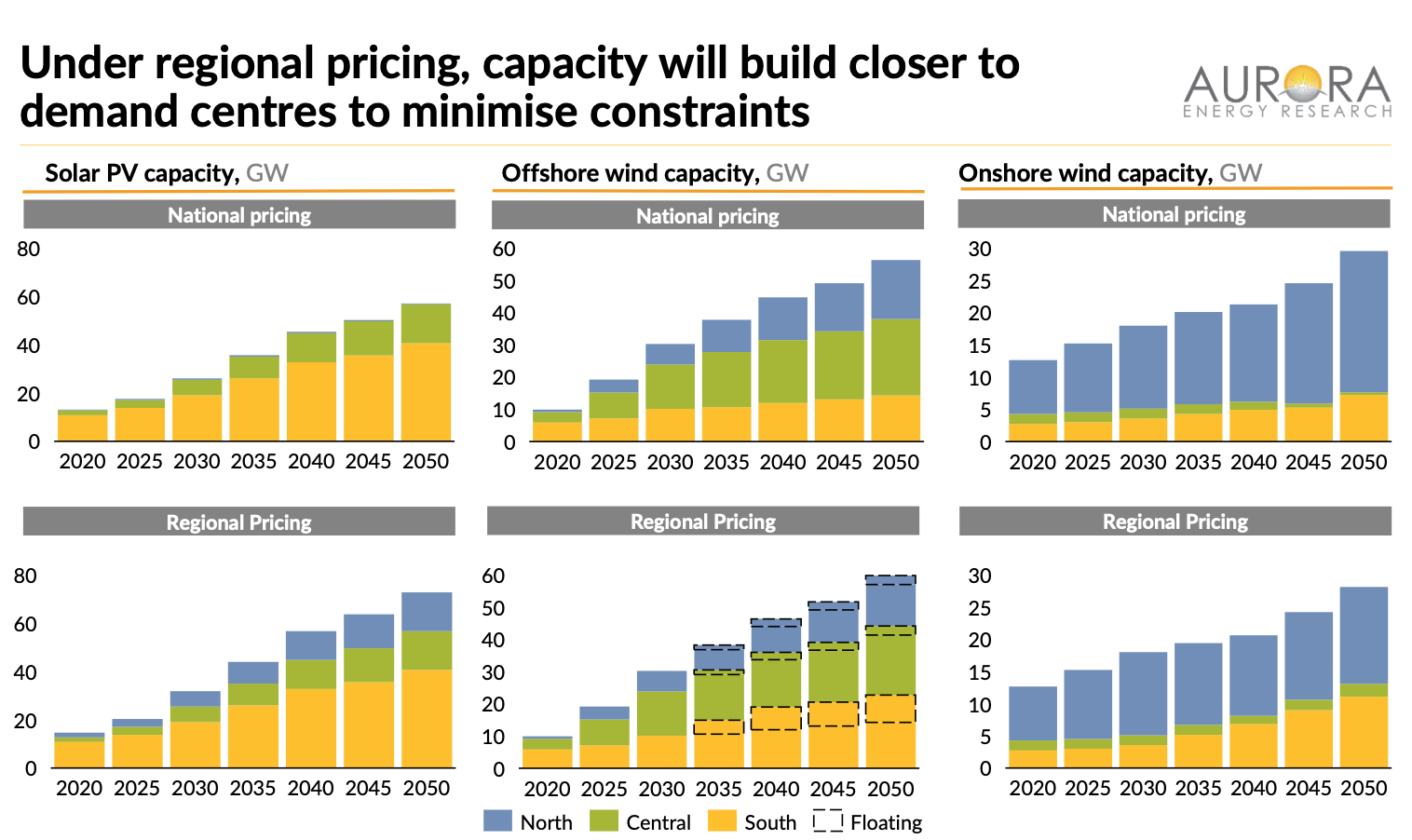

One of the effects of regional pricing is to increase the capacity of solar PV. Almost all (> 10 GW) of that extra PV is in Scotland (North, as they categorise it). We all know how sunny Scotland is, especially in winter. One of the main drivers of the increased demand for electricity is the electrification of heat. Demand for heat is very seasonal, particularly in Scotland. Solar output is very seasonal, especially in Scotland. Unfortunately, that is an inverse correlation. The extra PV in Scotland would be singularly useless for meeting the electrified heat demand. Admittedly, it would be quite useful for powering air-conditioning in the tropical parts of Scotland, but that is sadly a limited opportunity. It is not obvious that this is a cost-saving, efficiency-improving effect of regional pricing. If the model says it is, that says more about the model than about the potential for solar heating in Scotland.

Another key effect of regional pricing is the promotion of floating offshore wind capacity. It doesn’t exist at all under national pricing, which may be news to the developers of floating offshore projects. It seems likely that the addition of floating capacity under regional pricing was prompted by the need to explain how all the additional offshore capacity in the South will occur, rather than as a direct result of regional pricing.

In the South, the floating capacity is additive. In the Central (N England) and North (Scotland) zones, it is substitutive, i.e. displacing fixed offshore wind installations. In total, there seems to be 5-10 GW of additional offshore wind capacity as a result of regional pricing. But the increase in the South is double that, so there is a net reduction in offshore wind capacity in the other regions, and a larger reduction of fixed offshore wind, as some of it is substituted by floating systems. The GWPF has reported on the high cost of floating offshore wind.

It is (again) not obvious that the addition of (say) 20 GW of floating offshore wind, mostly in the South, and the removal of (say) 7 GW of fixed offshore wind in the North of England and Scotland is a cost-saving, efficiency-improving measure. Scotland may not have much sun in winter, but it has more wind than England. If the model indicates that it is cost-effective to increase offshore wind capacity and switch it from fixed installations in Scotland to floating installations in the South, then that (again) says more about the credibility of the model than about the efficiency of this option.

The last of the main effects of regional pricing on intermittent capacity (according to Aurora’s model) is to reduce the total capacity of onshore wind, and to relocate it from Scotland, mainly to the Southern region. That effect is so strong that the model suggests at best no increase at all in onshore wind in Scotland between 2030 and 2040, and apparently a slight reduction, while installation goes like gangbusters in the South.

One might freeze capacity for certain constraints, such as a combination of demand and network limitations. That is somewhat undermined by preceding and subsequent periods where the capacity increases, but it is conceivable. Why one would reduce capacity is hard to explain.

Only bad modellers think the job consists simply of constructing and running the model and reporting the outputs. Good modellers have the ability to do a subjective “sanity check” or “smell test” on preliminary runs of the model. This is a vital point at which one can spot an error in the design of the model. It is tempting to speculate that Aurora has too many PhDs, and not enough people with practical experience and common sense to spot when their models are not credible.

Onshore wind is the cheapest of the three intermittent technologies covered in Aurora’s chart above. Increasing solar and offshore wind whilst reducing onshore wind will not obviously save cost, any more than the previous measures.

Scotland has more wind than England, onshore as well as offshore. Load factors are a key component of the economics of wind. Wind projects located in the South will have materially lower load factors than those in Scotland, on average. Land values will be higher on average. There may be fewer obstacles getting the power to customers, but the electricity will not be cheaper, quite the reverse. And then there is the politics of a Conservative government encouraging a quadrupling of wind in the South whilst reducing its deployment in Scotland. Models have their limitations…

The charts say offshore wind will be around 30 GW in 2030. Government policy is 40 GW. The Conservative manifesto and government policy includes no matching ambition for the expansion of onshore wind and solar. The model assumes onshore wind and solar contribute around 55 of the 100 GW of extra wind and solar by 2050 in the default (national pricing) scenario, and more like 60 GW in the regional pricing scenario, most of it in the South, quadrupling the capacity of both in that region. Which Minister is going to volunteer to give the good news to the Conservative heartlands?

The reason that Aurora believe these changes will reduce cost is that “capacity will build closer to demand centres to minimise constraints”. This reinforces the political challenge. It begs the question of how offshore wind will build close to demand centres. Presumably, they will still be offshore, but perhaps technically closer, in the sense that the floating windfarms will connect into the grid further south than they otherwise would have done. Is the avoidance of an undersea backbone really worth the negatives described above of moving the windfarms further south and onto floating platforms?

It’s an odd conflation anyway, because the system problems created by an extra 100 GW of intermittent generation are not primarily to do with how close those GW are to demand. Supply and demand will be just as misaligned, wherever the windfarms are located. That means large amounts of storage will be required. If a lot of the output has to be taken into storage and then fed into the grid on demand, is the entry point to the grid the critical constraint? Cost of production will surely be more important, because the round-trip losses of storage exacerbate any cost differentials.

Is it really credible that this is about network constraints, when the combined capacity of wind and solar by region doesn’t change that much? The effect is not to move capacity south to reduce strains on the network. The effect is to move solar capacity north and wind capacity south. Presumably, the Aurora model has calculated that spreading the technologies more evenly is easier on the grid than concentrating the wind in the north and the solar in the south, even though that reflects the nature of the resources. Does Aurora’s model value correctly the geopolitical realities and the relative costs of transmission versus load factors?

The most credible elements of cost-saving in this aspect of the model are (a) the demand responsiveness of time-of-day pricing, and (b) a swing from wind (primarily offshore) to solar in the balance of intermittent capacity. But that is not what it says on the tin.

It’s a low blow, but deserved: if you had a good idea for electricity, you probably wouldn’t promote it on the basis that it’s how the Californians do it.

About the author

Bruno Prior joined his family company (Summerleaze) in 1988, the same year that they commissioned their first renewable power station. He has spent most of the time since then developing renewable-energy businesses. Those businesses included landfill-gas power generation and supplying renewable heating fuel. Summerleaze holds the increasingly unfashionable view that the risk of climate change does not supersede the need for our energy to be produced when we need it, as cheaply as possible.

Bruno's experiences of a nationalised energy sector, and then (since privatisation) of the descent into ever greater corporatism, inept policy design, and regime uncertainty, lit a passion for classical-liberal economics, which led him to the Institute of Economic Affairs, where he is now a trustee. He is writing here in a personal capacity.