New data on offshore wind costs

A series of reviews of the financial accounts of offshore windfarms has shown that despite the claims of the offshore wind industry, overall costs of offshore windfarms remain stubbornly high, and are at best only declining slowly.

One of those studies was published by GWPF using data to 2019. This post updates those estimates based on the latest data: 2020 audited financial accounts, and the equivalent generation data from Ofgem.

Since the original report was published, the Hornsea 1 and East Anglia 1 windfarms have gone into full production. Hornsea 1 came in well over budget – indeed, at £4.1m/MW capacity, it is amongst the most expensive offshore windfarms (in £/MW capacity terms) in the UK to date. This is likely to be due to it being much further offshore than previous developments, as well as being in relatively deep water. East Anglia 1 is rather cheaper, at £3.6m/MW capacity.

The 2020 financial accounts also give us a chance to better estimate the build cost of Moray East, which installed its final turbine a few weeks ago. Moray East is one of the most interesting windfarms, because of its very low Contract for Difference bid. Currently worth £69/MWh, much lower than any previous windfarm, this has been taken to indicate the start of a revolution in offshore wind costs. However, the windfarm’s 2020 accounts reveal that it had spent £2.2 billion by the end of last year, before incurring its major capital cost, namely the wind turbines themselves. This means that the final cost is unlikely to be less than £3.8 billion, or £4m/MW, similar to Hornsea 1.

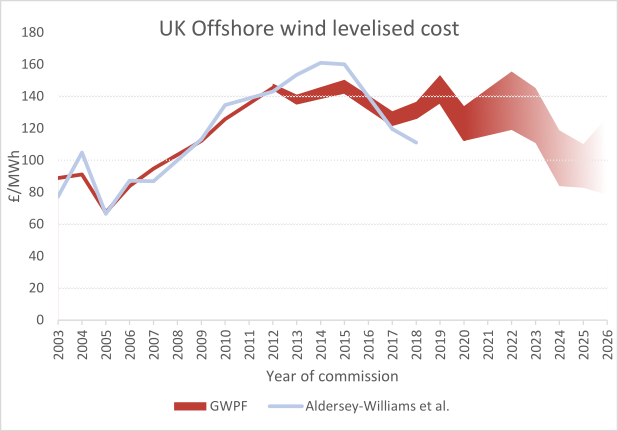

It is fair to say that as well as increasing capital costs, moves to deeper waters have brought slightly better load factors for offshore windfarms. But the extra costs involved in doing so appear to have largely wiped out those gains. The figure below shows GWPF’s current estimate of the levelised cost of offshore wind power,* together with the earlier estimate published by Aldersey-Williams et al. In both cases, the values shown are capacity weighted averages, with the GWPF range (in red) representing optimistic and pessimistic views of future costs.

Costs seem to have been approximately level from 2013–2019. East Anglia 1, coming in on budget in 2020 and delivering expected performance, has produced a sharp fall for that year, but costs for the next three windfarms to come on stream (Triton Knoll, Moray East, and Hornsea 2) look as though they will return to normal levels.

The announced costs for windfarms after 2024 do suggest a reduction in levelised costs, but only to around the £100/MWh mark. These reductions are due to the Dogger Bank windfarms, which are being built in shallow waters. However, they are also far offshore - up to 200km. The best guide we have as to the effect of such distances on costs is Hornsea 1, which, as we have seen, has turned out very expensive. So it would not be at all surprising if these huge windfarms turned out to be no cheaper at all.

Even if the Dogger Bank windfarms do turn out to be able to generate power at £100/MWh, electricity in the UK will still become disastrously expensive. The Climate Change Committee is suggesting that costs will have fallen to less than half that level by 2050, based on the low Contracts for Difference bids received in recent years. But there is wide agreement (windfarm promoters excepted) that CfD results are not a good guide to underlying costs. The Oxford Energy Institute notes that despite the low CfD auction results, in international technology cost reports "there is insufficient evidence for such a steep decline [in costs]". Aldersey-Williams et al say that "offshore wind farm costs are still much higher than those implied by recent bids for UK government financial support via Contracts for Difference (CfDs)". Hughes notes that CfDs can be cancelled with relatively small penalties, suggesting that that windfarm developers may be banking on taking higher open-market prices at some point.

The government is relying on a revolution in offshore wind costs to make Net Zero more affordable. Minister have claimed that it has happened already. But If it it doesn't happen, the cost to consumers will run into hundreds of billions of pounds. And unfortunately the hard evidence set out here shows that it is not happening.

We wrote to Kwasi Kwarteng to explain the risk. We wrote to the Net Zero Review team at the Treasury too. But both ministers and officials seem determined to ignore or brush such concerns aside.

*As always when using levelised costs, it should be noted that this refers only to costs at generator level. The cost of dealing with the intermittency of wind power is not included.